- Series I bonds, an inflation-protected and nearly risk-free investment, may soon pay an estimated 9.62%, according to experts.

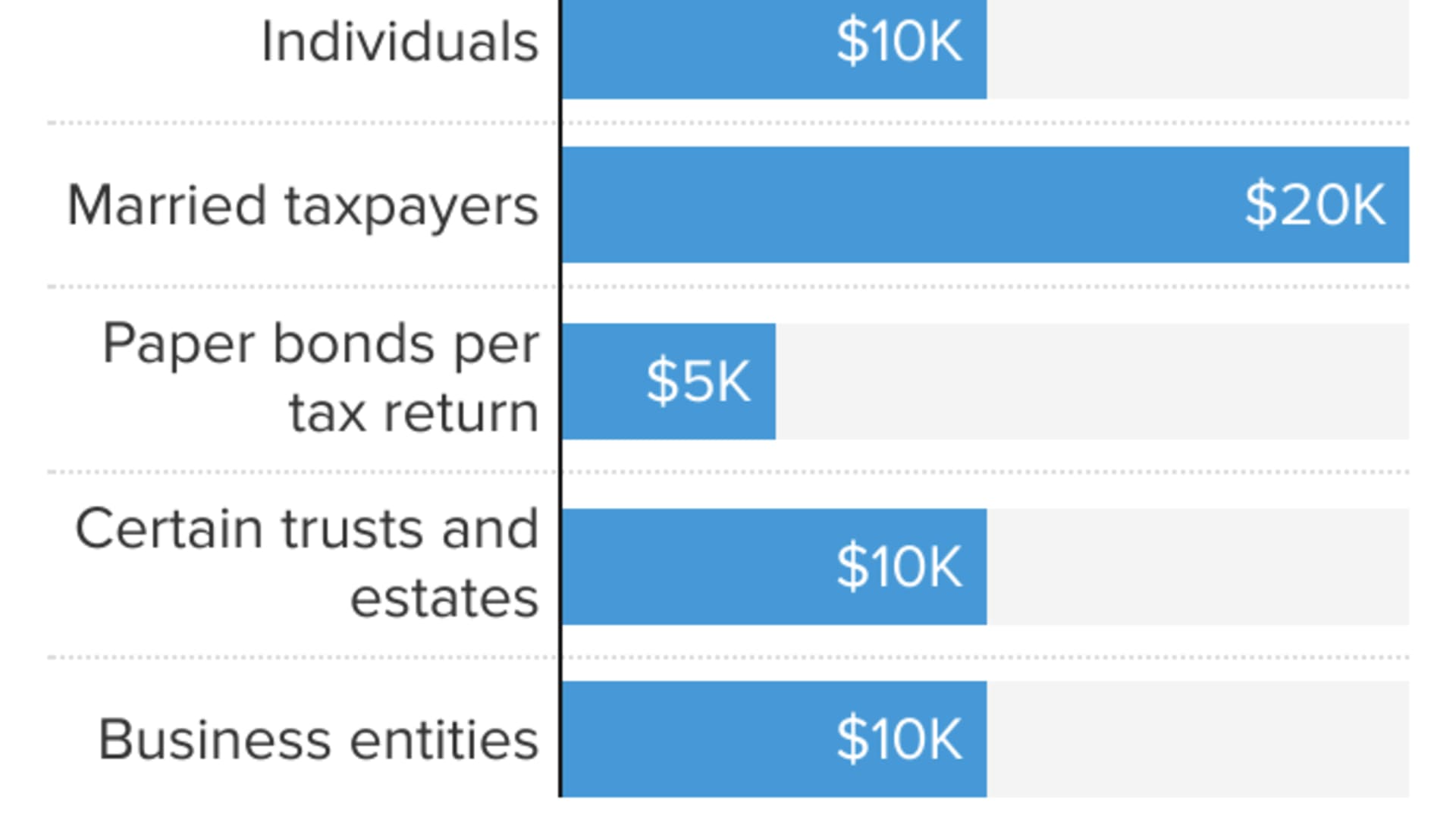

- While there’s a $10,000 limit for individuals per calendar year, there are a few ways to buy more.

- However, there are some downsides to consider before purchasing, such as locking up funds for one year.

Less risk often means lower returns. But that's not the case with Series I bonds, an inflation-protected and government-backed asset, which may soon pay an estimated 9.62%.

I bonds currently offer 7.12% annual returns through April, and the rate may reach 9.62% in May based on the latest consumer price index data. Annual inflation grew by 8.5% in March, according to the U.S. Department of Labor.

"The 9.62% is an eye-watering number," said certified financial planner Christopher Flis, founder of Resilient Asset Management in Memphis, Tennessee. "Especially given how other fixed-income assets have performed this year."

Get a weekly recap of the latest San Francisco Bay Area housing news. Sign up for NBC Bay Area’s Housing Deconstructed newsletter.

Of course, the 9.62% return is an estimate until the U.S. Department of the Treasury announces new rates on May 2. Still, I bonds may be worth a look if you're seeking ways to beat inflation. Here's what to know before buying.

How I bonds work

Money Report

I bonds, backed by the U.S. government, won't lose value and pay interest based on two parts, a fixed rate and a variable rate, changing every six months based on the consumer price index.

If you purchase I bonds by the end of April, you'll lock in 7.12% for the next six months, followed by an estimated 9.62% for another six months, for a 12-month average of 8.37%, according to Ken Tumin, founder and editor of DepositAccounts.com, who tracks these assets.

However, there are only two ways to purchase these assets: online through TreasuryDirect, limited to $10,000 per calendar year for individuals or using your federal tax refund to buy an extra $5,000 in paper I bonds. There are redemption details for each one here.

You may also buy more I bonds through businesses, trusts or estates. For example, a married couple with separate businesses may each purchase $10,000 per company, plus $10,000 each as individuals, totaling $40,000.

Downsides of I bonds

One of the drawbacks of I bonds is you can't redeem them for at least one year, said George Gagliardi, a CFP and founder of Coromandel Wealth Management in Lexington, Massachusetts. And if you cash them in within five years, you'll lose the previous three months of interest.

"I think it's decent, but just like anything else, nothing is free," he said.

Another possible downside is lower future returns. The variable portion of I bond rates may adjust downward every six months, and you may prefer higher-paying assets elsewhere, Gagliardi said. But there's only a one-year commitment with a three-month interest penalty if you decide to cash out early.

Still, I bonds may be worth considering for assets beyond your emergency fund, Flis from Resilient Asset Management said.

"I think that the I bond is a wonderful place for people to put the money they don't need right now," he said, such as an alternative to a one-year certificate of deposit.

"But I bonds aren't a replacement for long-term funds," Flis said.