- Many Americans would have had a hard time paying an unexpected $400 expense, even before the Covid-19 pandemic.

- After three stimulus checks, many Americans were able to build up some of their cash reserves.

- But whether or not those balances stay remains to be seen.

Many Americans were financially squeezed even before the Covid-19 pandemic began.

As of 2019, 41% of households ages 25 to 64 said they did not have enough saved to cover an unexpected $400 expense, according to Federal Reserve data.

One reason they may have had trouble setting aside cash: persistent credit card debts.

Get a weekly recap of the latest San Francisco Bay Area housing news. Sign up for NBC Bay Area’s Housing Deconstructed newsletter.

Then the pandemic upended many Americans' financial situations.

More from Personal Finance:

Collecting unemployment? Most states re-impose 'look for work' rules

What to know about the new eviction ban

More workers plan to quit as better job opportunities open up

The unexpected upheaval prompted the U.S. government to send an unprecedented amount of direct cash payments to millions of Americans.

Money Report

The Center for Retirement Research at Boston College looked at whether those cash infusions have helped improve Americans' financial situation.

The answer: Stimulus checks did serve as a lifeline for those in need. But whether those cash reserves will hold remains to be seen.

Congress authorized the first stimulus checks of $1,200 per person in March 2020. Subsequent payments of up to $600 and $1,400 followed in December and this past March, respectively.

In total, individuals could have received up to $3,200 and married couples up to $6,400. In addition, there was up to $2,500 available per qualified dependent. While eligibility rules varied per payment, whether or not individuals were employed at the time was generally not a qualifier.

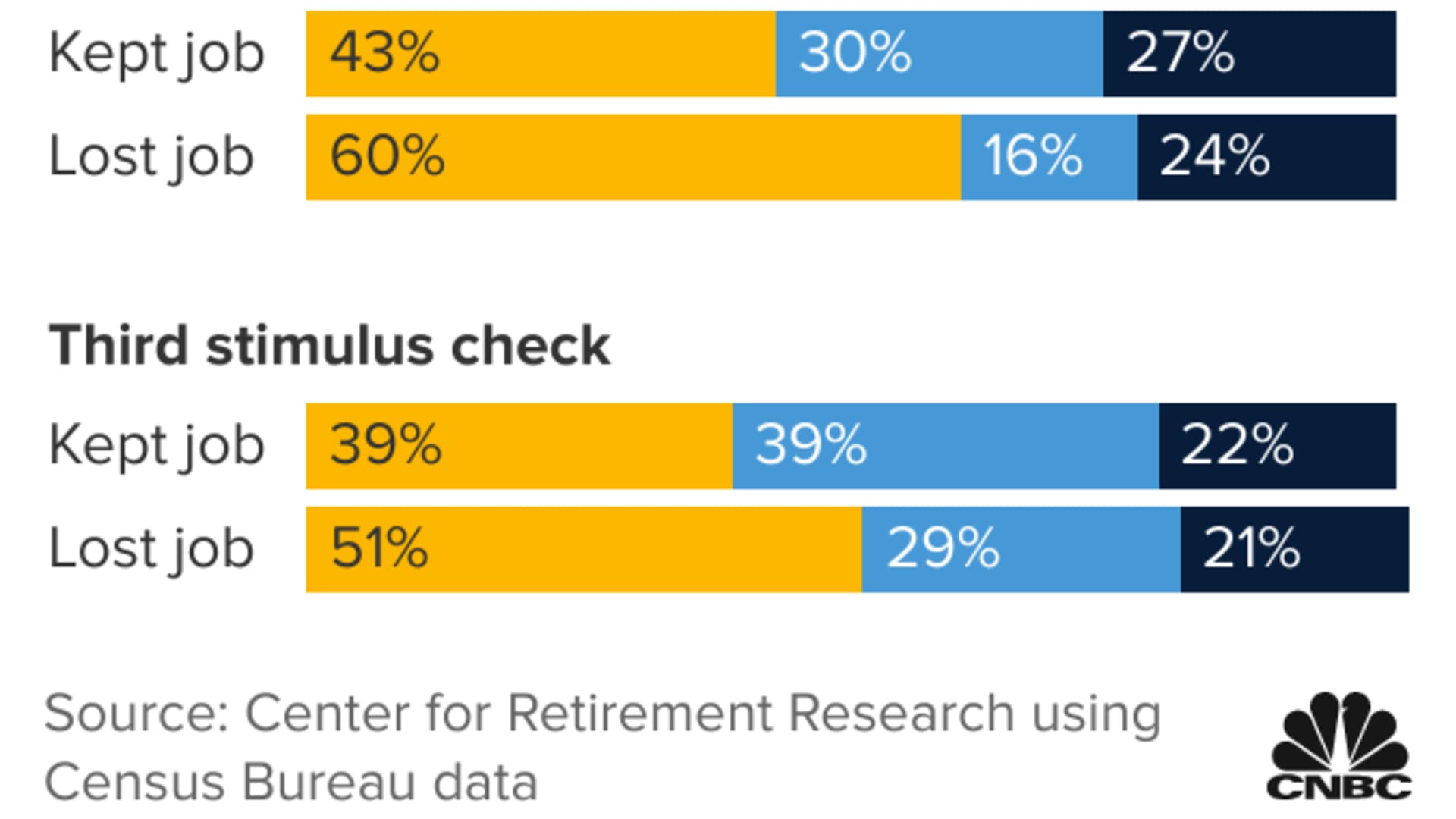

And it seems employment was indeed a factor in whether those checks changed a household's ability to cover a $400 expense. For people who kept their jobs, those who still had trouble handling a $400 expense dropped to about one-third and stayed there throughout 2020.

For those who lost their jobs, however, that fluctuated. In April 2020, about 51% would have had trouble covering a $400 expense, which dropped to 36% in June 2020 as a result of the direct payments. That rate rose again as of November 2020, when 55% of those who were jobless again would have had trouble with a $400 emergency, as the extra $600 per week in federal unemployment benefits had run out and Congress was at a stalemate over more stimulus relief.

How households used the money also varied based on employment status. Unsurprisingly, those who kept their jobs were able to pay down their debts and save.

For those who lost their jobs, the first $1,200 stimulus checks were mostly spent. However, the second and third payments were mostly devoted to saving, at 60% and 51%, respectively, with recipients using the majority of the second $600 and third $1,400 stimulus checks to set aside cash.

"The question is how long these favorable balance sheet developments will last," the Center for Retirement Research report states.

Keeping high interest credit card debt in check, which precluded people from setting aside money before the pandemic, could help. Notably, reducing debts was a priority for many Americans — both jobless and employed — for the second and third stimulus checks.

However, the latest data from the Federal Reserve shows household debt is on the rise, with credit card debts rising by $17 billion in the second quarter. Despite that increase, credit card balances were still $140 billion less than they were as of the end of 2019.