Americans in their 50s are right around the corner from reaching retirement age, but don't have much saved up for their post-work years.

By the time you reach your 50s, you should have around six times your salary saved for retirement, according to Fidelity Investments, the largest 401(k) provider in the U.S. If you earn around $100,000 annually, you'd ideally have $600,000 saved for retirement by the time you reach your 50s.

However, many people in that age range have less than half of that in their 401(k)s.

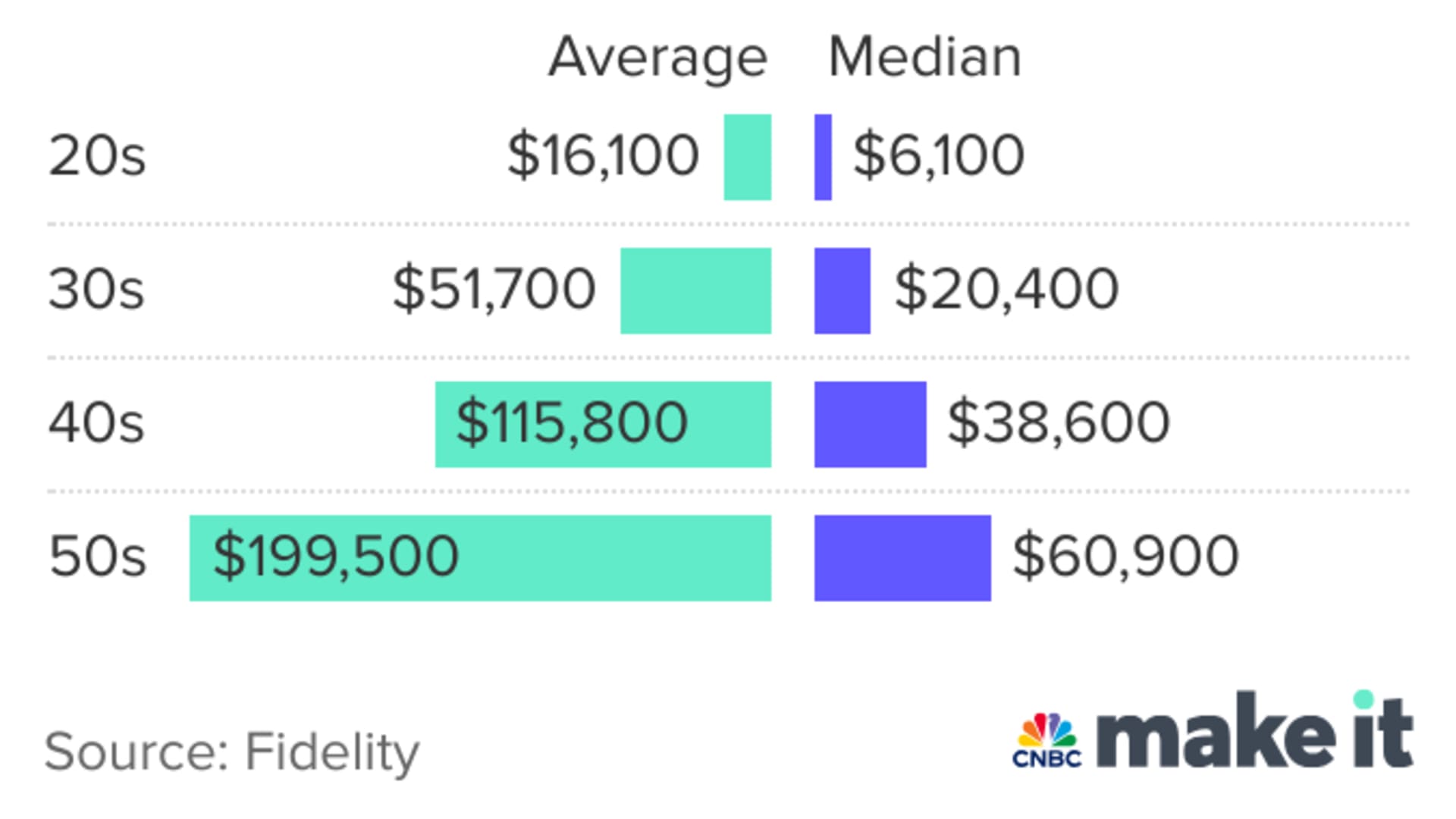

The median 401(k) account balance for Americans in their 50s is $60,900 as of the last quarter of 2023, per Fidelity data provided to CNBC Make It. The average account balance is $199,500, but a few larger account balances can skew the average to be higher.

Get a weekly recap of the latest San Francisco Bay Area housing news. Sign up for NBC Bay Area’s Housing Deconstructed newsletter.

Here's how much Americans have in their 401(k)s by age as of the fourth quarter of 2023, according to Fidelity.

One reason people in their 50s tend to fall short with their retirement savings is because they didn't get to benefit from relatively recent changes to the 401(k) system, says Anne Lester, a retirement expert and author of "Your Best Financial Life: Save Smart Now for the Future You Want."

Money Report

While many younger workers have benefited from updates like auto-enrollment, which automatically enrolls you in your employer's 401(k) plan, and auto-escalation, which automatically increases your savings rate by a given amount each year, many older workers were well into their careers by the time these changes became widely adopted, she tells CNBC Make It.

"Gen Xers had to make a decision when they were entering the workforce about whether they want to participate in their employer's retirement plan, and participation rates were typically low back then," Lester says. "But when people are automatically enrolled, participation rates are usually around 95% because people don't drop out."

The good news is that among all of the age cohorts, people in their 50s have the highest savings rate, which is the percentage of your income allocated toward retirement savings. They put around 13% of their income toward retirement, inclusive of employer matches, which is just shy of Fidelity's recommended 15%.

How to get your retirement savings on track

If you're in your 50s and feel behind on your savings, don't panic. You have a few options available to you.

Retirement catch-up contributions

Americans in their 50s and beyond have the opportunity to make "catch-up" contributions, which are extra deposits you can make toward tax-advantaged retirement savings plans.

For the 2023 and 2024 tax years, anyone 50 and older can contribute up to $7,500 in additional funds to their 401(k). They can also contribute up to $1,000 extra to a traditional or Roth individual retirement account.

Delaying retirement by a few years

If you're very far behind in your savings, it may be time to reconsider the age you plan to retire, Lester says.

"In your 50s is when you should start thinking 'OK, let's get real about this,'" she says. "It's time to start planning and understanding what your post-retirement income may look like under various scenarios, such as if you stopped working at 62, at 65, at 67 or at 70."

"Working longer is great because you can save more, but also, you actually need a lower level of savings to last because your retirement is shorter," Lester adds.

Additionally, delaying retirement gives your savings more time to grow.

Taking Social Security benefits later

You can begin receiving your Social Security retirement benefits when you turn 62, but your payout is permanently reduced if you start receiving benefits before your full retirement age, as determined by the Social Security Administration.

"Just waiting a few years gives you a huge boost to your guaranteed inflation-adjusted income in retirement," Lester says. "It really pays to delay."

For every year you delay between your full retirement age and age 70, your Social Security benefit increases by 8%.

What to do if you can't delay retirement

However, not everyone can or wants to delay their retirement.

If that's the case, you may need to figure out how you're going to live on less money during your post-work years, Lester says.

Once you've got a clear picture of how much money you'll have to take care of yourself after you stop working, you can begin figuring out how to reduce your spending.

"It's really constructive to get curious about where your financial line is," Lester says. "There's a floor you don't want to go underneath, but there's also a level of reduced spending you can get used to."

If you're planning to live on a smaller annual income during retirement, you may want to research moving to places with a lower cost of living or plan to cut certain discretionary expenses ahead of time.

"The earlier you start mentally making that shift, the less painful it will be when you start having to do it," Lester says.

Want to make extra money outside of your day job? Sign up for CNBC's new online course How to Earn Passive Income Online to learn about common passive income streams, tips to get started and real-life success stories. Register today and save 50% with discount code EARLYBIRD.

Plus, sign up for CNBC Make It's newsletter to get tips and tricks for success at work, with money and in life.